Just last month, China sent astronauts into space to board a new space station. Earlier this year, China landed a rover on Mars. Chinese state media reported that inside both China’s space station and the Mars rover were 100% indigenously designed-and-produced semiconductors, signaling China’s increasingly sophisticated microchip capabilities.

Nevertheless, while China has mastered some chip technologies, its commercial semiconductor industry is still relatively nascent. Still, the Chinese government is making serious efforts to close the gap, investing well over $150 billion from 2014 through 2030 in semiconductors. Buoyed by a booming market and these government investments, China is poised to be increasingly competitive in some semiconductor market segments.

In order to form a calibrated and appropriate U.S. policy response, it is important to examine China’s current place in the semiconductor supply chain, what its prospects are, and what aspects of China’s semiconductor industrial policy may pose challenges. Ultimately, the winning formula for long-term competition with China is to invest in American semiconductor technology and to strengthen the resiliency of America’s chip supply chains.

I. China’s Important Role in the Global Electronics Supply Chain

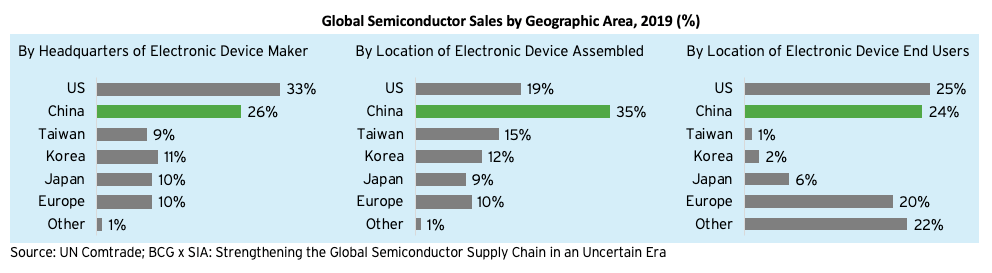

China is the world’s largest manufacturing hub, producing 36% of the world’s electronics – including smartphones, computers, cloud servers, and telecom infrastructure – cementing the country as the largest node in the global electronics supply chain. In addition, with nearly one-fifth of the world’s population, China is the second-largest final consumption market – after the U.S. – for electronic devices embedded with semiconductors.

The driving force behind these dynamics is a highly global semiconductor and ICT supply chain, where indigenous Chinese and multinational contract electronics manufacturers based in China import semiconductors that are then assembled into tech products to be re-exported or sold in the domestic market for final consumption. To underscore this point, in 2020, China imported a whopping $378 billion in semiconductors; assembled 35% of the world’s electronic devices; accounted for 30% to 70% (depending on the product) of the global TV, PC, and mobile phone exports; and consumed one-quarter of all semiconductor-enabled electronics. Access to this massive market is essential to the success of any globally competitive chip firm today and in the future.

As a latecomer to the semiconductor sector, the indigenous Chinese chip industry is relatively small, accounting for only 7.6% of total global semiconductor sales. Chinese chip firms primarily sell discrete semiconductors, lower-end logic chips, and analog chips to consumer, communications, and industrial end markets. Chinese chip firms are notably absent in the market for high-end logic, advanced analog, and leading-edge memory products. China’s indigenous semiconductor supply chain is even less developed. It lags significantly in advanced logic foundry production, EDA tools, chip design IP, semiconductor manufacturing equipment, and semiconductor materials. Chinese foundries currently focus on more mature nodes, and China’s supply chain capabilities at the equipment and materials level are presently limited to older technologies.