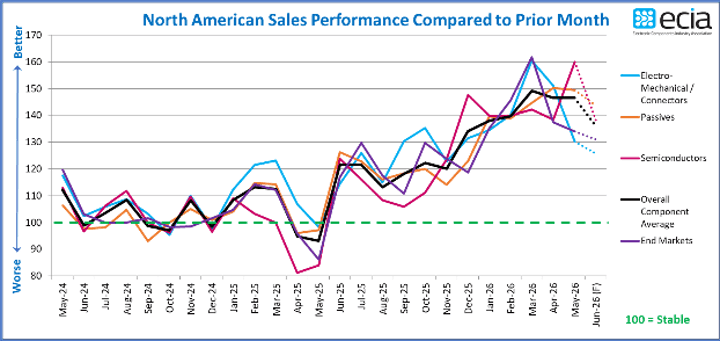

Atlanta – Contrary to weakening expectations in the April Industry Sentiment Survey, May results reveal that overall sales sentiment sustained strong results once again. May’s overall sales sentiment remained unchanged from April at a robust 146.6. Unfortunately, the solid May results give way to lingering concerns as the overall average drops by 10.8 points in the June forecast.

“Every segment is expected to see a significant drop in sales sentiment in June,” commented ECIA Chief Analyst Dale Ford. “HOWEVER, this result shows some cognitive dissonance with the quarterly results from the Q2 Industry Pulse survey. The overall average expectation for growth among survey respondents was 70% for Q2 and jumped to 79% in the Q3 forecast. Among survey respondents in the current Q2 survey, 32% expect growth in Q2 above 3% and 44% see growth above 3% in Q3.”

ECIA’s Industry Pulse: Electronic Component Trends and Sentiment provides highly valuable and detailed visibility on industry expectations in the near-term through the monthly and quarterly surveys. This “immediate” perspective is helpful to participants up and down the electronics components supply chain.

The complete ECIA Industry Pulse: Electronic Component Trends and Sentiment Report is delivered to all ECIA members as well as others who participate in the survey. All participants in the electronics component supply chain are invited and encouraged to participate in the report so they can see the highly valuable insights provided by the Industry Pulse: Electronic Component Trends and Sentiment report. The return on a small investment of time is enormous! Members can log in here to see the full report.

The monthly and quarterly Industry Pulse: Electronic Component Trends and Sentiment reports present data in detailed tables and figures with multiple perspectives and cover current sales expectations, sales outlook, product cancellations, product decommits and product lead times. The data is presented at a detailed level for six major electronic component categories, six semiconductor subcategories and eight end markets. Also, survey results are segmented by aggregated responses from manufacturers, distributors, and manufacturer representatives.