SOURCE: SEMI Blog

Authors: Ajit Manocha and Sanjay Malhotra

Global semiconductor supply imbalances have hindered countless industries including essential segments such as automotive and medical as well as workers and consumers. Around the world, policymakers are increasing semiconductor manufacturing capacity to strengthen supply chains and meet growing demand for semiconductors through robust incentive packages totaling hundreds of billions of dollars. This global effort to grow semiconductor manufacturing capacity hinges on the production and installation of additional semiconductor manufacturing equipment (SME). Simply put, without more SME, there can be no additional capacity.

Chip shortages have contributed to increased lead times for fab equipment and other complex semiconductor manufacturing tools. Lead times for fab equipment were between three to six months in 2020, extending to 10 months on average in the first quarter of 2021, and even further to 14 months on average in July of 2021. For some fab equipment, the lead time exceeds two years.[1]

Ensuring chip supplies needed for SME will significantly reduce lead times for the fab equipment that semiconductor device makers need to expand capacity without changing their allocation strategies.

All Efforts to Expand Chip Production Depend on SME

Extended lead times for equipment are holding back marginal fab expansions where space is readily available to add capacity and could significantly hamper expansion efforts for a wide range of device makers and their supply chain – from materials and process equipment suppliers through packaging and test providers. According to the SEMI World Fab Forecast, 86 new fabs or major fab expansions are expected to come online between 2020 and 2024 (see Figure 1), representing 20% growth in total 200mm fab capacity and 44% growth for 300mm capacity over this period. Longer delivery times for equipment mean a slower ramp-up of planned chip production capacity, potentially prolonging the shortage.

Figure 1: New 300mm and 200mm fabs expected to come online from 2020-2024 by region

The production of SME is dependent on a relatively small volume of semiconductors that are often purchased and incorporated into SME components by contract manufacturers to the SME original equipment manufacturer (OEM). These chips for SME OEMs and contract manufacturers account for far less than 1% of the global semiconductor market.[2] However, the chips for SME are essential to increasing semiconductor production capacity and meeting growing demand, making them critical to the success of all investments and public policies designed to increase capacity and strengthen the manufacturing supply chain.

The immediate challenge to expanding SME production is ensuring an adequate, timely and reliable supply of semiconductors. Additionally, silicon substrates are equally crucial for semiconductor production. Raw wafer producers also rely upon SME to increase capacity, and this equipment also requires chips. Industry and government stakeholders calling for capacity growth must make sure SME OEMs and contract manufacturers receive the chips they need to build the tools essential to ramping new fabs.

The SME Multiplier Effect

Importantly, while the volume of semiconductors required to build SME are very small, these tools enable the production of a very large number of chips, equating to a >1000x multiplier effect.[3] SME OEMs require various quantities and types of semiconductor devices – such as field programmable gate array (FPGAs), power management ICs (PMICs), sensors, microcontroller units (MCUs), programmable logic devices (PLDs), analog to digital converters, power amplifiers and memory chips – for their different tools. The multiplier effect applies to all tools; some examples include:

- A typical FPGA test tool requires approximately 80 FPGAs to build. However, that tester can then test about 320,000 FPGAs per year – a multiplier effect of ~4,000x.

- Process tools require about 100 FPGAs to build and can process 120 or more wafers per hour. Wafers make many passes through each tool during the manufacturing flow but the share of most tools’ contribution to overall production equates to at least 2 million devices per year – a ~20,000x multiplier.

- Optical wafer inspection tools require roughly 100 high performance computing (HPC) server chips to manufacture. Their multiplier effect can be ~30,000x and much higher.

- A typical MCU Tester needs approximately 100 FPGAs to be manufactured, but that tool can then test nearly 10 million MCUs in a year, a multiplier effect of ~100,000x.

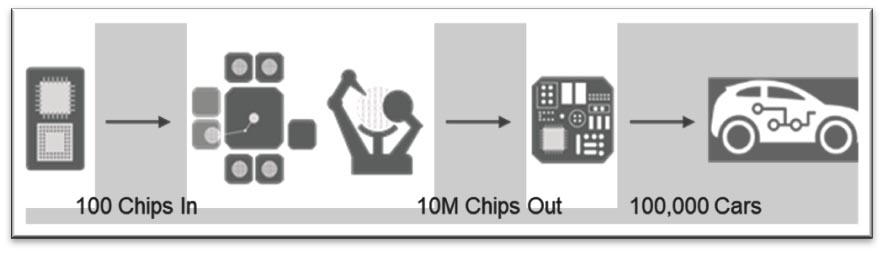

The U.S. Commerce Department has noted that MCUs are among the chips facing the most acute shortages.[4] They are used in many key downstream industries including automotive. If we consider an example using a 100,000x multiplier effect for a tester and extend it to the automotive supply chain, assuming the number of MCUs required for auto manufacturing is ~100 per car, every tool/tester enables enough MCUs to build 100,000 cars (see Figure 2).

Figure 2: Example of the SME chip multiplier effect’s impact in the automotive market (Source: SEMI research)

This MCU tester example demonstrates the strong multiplier effect of ensuring an adequate supply of chips for SME OEMs and contract manufacturers. To increase capacity, the semiconductor industry needs more SME. What’s more, automakers and companies in other industries depend on the capacity growth that SME enables. The production of billions of semiconductors and countless downstream devices incorporating semiconductors ultimately rely on a small number of chips used in SME. All stakeholders in the semiconductor supply chain must help ensure adequate supplies of these chips so that semiconductor production capacity can grow to meet future needs and supply chains are strengthened to avoid future shortages.

Conclusion

Semiconductor device manufacturers face a daunting challenge as they work to equitably allocate chips to essential industries such as automotive and medical, yet it is crucial to raise awareness of the chip shortage faced by SME OEMs. With the small chip-volume requirements for SME, prioritizing chips for vital semiconductor manufacturing tools will not require device makers to change their allocation strategies, resulting in wins all around – from SME OEMs and semiconductor device makers to end-market OEMs and ultimately consumers.

Without the essential contributions of SME, expanding fab capacity to enable greater semiconductor production needed for countless downstream industries will not be possible. The payback for prioritizing chips for SME is immense. The resulting reduction in equipment lead times will enable dramatic increases in semiconductor production capacity, help mitigate chip shortages and improve ROI.

[1] Source: Various SME OEMs

[2] Various SME OEMs

[3] The SME multiplier effect and examples are based on research conducted by SEMI with input from SME OEMs.[4] https://www.commerce.gov/news/blog/2022/01/results-semiconductor-supply-chain-request-information

Ajit Manocha is president and CEO and Sanjay Malhotra is vice president of corporate marketing and the market intelligence team at SEMI.