The Japanese data centre ecosystem has a long-standing reputation as one of the most stable and mature markets in the world. However, as with other markets focused on a traditional hub, such as those in FLAP-D, there are early signs that demand may be starting to shift away from its core in Tokyo.

One market that could benefit is Kyushu. Japan’s most southerly island, home to the major cities of Fukuoka and Nagasaki, has seen an uptick in interest from hyperscalers over the past two years. DC Byte’s analysts explain the early signals and unpack what could make Kyushu an attractive future market for hyperscalers, operators, and investors.

DC Byte Market Analytics map search

Early Signs in Kyushu

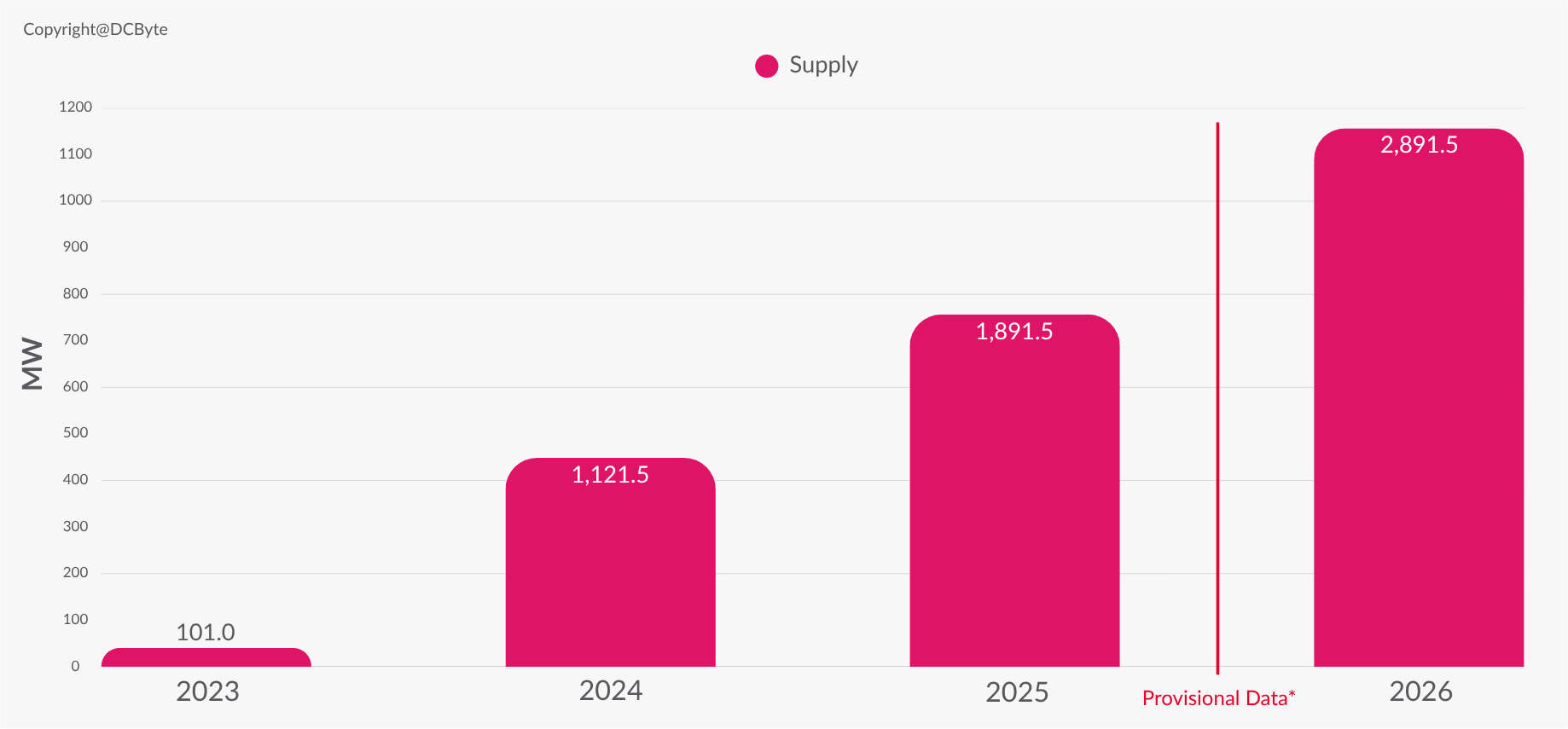

As of June 2026, Kyushu is a small market, with around 21 MW of live capacity. However, the island is showing early signs of transformation. Kyushu’s planned capacity has rocketed since 2023, rising from approximately 101 MW to around 3 GW at the time of writing. Much of this planned capacity originates from hyperscalers and major operators, demonstrating growing interest in the market.

Of course, these early signs come with a significant caveat. Although interest is strong, very little of Kyushu’s pipeline has yet entered the construction phase. This means that a portion of this interest is likely to be speculative and may never be converted into live capacity. Nevertheless, early indications are that Kyushu is a market to watch in the coming years.

Cumulative Supply in Kyushu

Escaping Tokyo Traffic

Tokyo retains its position as Japan’s core market for demand. The city is one of the world’s major business and finance capitals, and benefits from well-established infrastructure and subsea cables connecting it to the Americas and the rest of APAC. These factors have traditionally made Tokyo attractive to hyperscalers and any business that needs low-latency workloads and a ready-built consumer market.

However, despite high demand, growth in the Tokyo Bay area has steadied since 2024. Like mature markets across the globe, Tokyo is experiencing constraints, including:

- Power delays: A commercial power connection in Tokyo can take as long as 8–10 years, in contrast to half or a third of that time in other regions of Japan.

- Construction bottlenecks: Although construction bottlenecks are a constraint on delivery timelines across Japan, the problem is particularly pronounced in Tokyo due to demand.

- Land costs: Central and western Tokyo have become prohibitively expensive for many operators and developers, especially for the large plots of land required by hyperscalers.

Combined, these factors appear to be driving early interest in alternative Japanese markets such as Osaka and Kyushu.

The Role of Power Prices

Although not the most expensive in Japan, Tokyo’s commercial power costs sit firmly in the country’s median price range at ¥25 to ¥33 per kWh. By contrast, Kyushu offers some of the cheapest energy costs in the country, often 10–15% lower than those in eastern Japan.

Alongside this, Kyushu benefits from a ready supply of renewable energy, leading the nation in both geothermal and solar generation. Due to its high volcanic activity, some estimates attribute 40% of Japan’s renewable energy production to the island. For hyperscalers and operators searching for cheaper power, and looking to burnish their sustainability credentials, this makes Kyushu an attractive proposition.

An Abundance of Land

In contrast with the Tokyo Bay area, Kyushu possesses an abundance of reasonably priced land close to major cities like Nagasaki and Fukuoka. The availability of relatively cheap land has catalysed an interesting trend among hyperscalers.

The Japanese market has traditionally been dominated by colocation development. In core markets like Tokyo, space is at a premium and land is expensive, meaning it is often more cost-effective for hyperscalers and international operators to lease capacity from colocators.

However, 88% of the planned projects on Kyushu are self-builds. This is due to the relative ease of securing power and land in Kyushu compared with the major metros, where few such opportunities exist. It’s important to state that this is merely an early signal, and the market in Kyushu does suffer from the same construction constraints as the rest of Japan. However, it could point the way towards hyperscalers exploring alternatives to colocation.

Geographic Factors

Kyushu’s position in the southwest of Japan offers some geographic advantages to developers and operators. The island is closer to East Asian business hubs like Seoul and Shanghai than it is to the capital, Tokyo.

In addition, it benefits from extensive submarine cables to South Korea, China, and the rest of the Asia Pacific region. This makes it an ideal strategic hub for cross-border workloads such as cloud regions.