By Dieter Weiss, in4ma

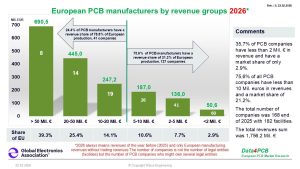

Is it time to celebrate that the European PCB manufacturing industry grew by 2.4% in 2025? Definitely not, when at the same time the global PCB market increased by more than 11%. The general negative trend for Europe is unbroken. Only due to a devaluation of the USD against the Euro does it look as if Europe grew by 6.9% on USD-basis. The total number of PCB manufacturers declined by 11 companies in 2025 to 168 manufacturers with 182 facilities. For 2026 we are now counting two more companies with TLT-PCB coming online and a Swedish OEM having started inhouse manufacturing of PCBs.

Is it time to celebrate that the European PCB manufacturing industry grew by 2.4% in 2025? Definitely not, when at the same time the global PCB market increased by more than 11%. The general negative trend for Europe is unbroken. Only due to a devaluation of the USD against the Euro does it look as if Europe grew by 6.9% on USD-basis. The total number of PCB manufacturers declined by 11 companies in 2025 to 168 manufacturers with 182 facilities. For 2026 we are now counting two more companies with TLT-PCB coming online and a Swedish OEM having started inhouse manufacturing of PCBs.

Looking at the product types, there is not too much movement with rigid-flex and flexible Multilayers show a positive trend. For the market segments we see a strong decline in automotive, which was expected. Medical electronics are down as well. The biggest market sector is still industrial electronics, which is characterized by high mix and low volume products which are manufactured in Germany with about 46% of PCB for this segment. The industry segment grew by more than 43 mil. €. In absolute terms, the biggest winner in 2025 is defense electronics with a plus of 23% and more than 50 mil. €. Air & Space Electronics, which on European level has been separated from defense electronics, grew by 15%, which equals nearly 23 mil. €.

France is leading the defense electronics segment with about 41%, followed by Great Britain with more than 28%. Air & Space electronics is dominated by Italy with 33.5%, followed by France/Belgium. Medical electronics seem to be the preferred market for Swiss PCB manufacturers which, together with Austria have more than 70% of this segment.

Germany has now seen a decline of their PCB manufacturing revenues for three consecutive years. Since 2022 they lost more than 27% of manufacturing revenues, whereas Austria and Switzerland saw an increase in business by more than 6% in the same period. A strong 32% growth from 2022 to 2025 can be seen as well in France/Belgium and revenues per head show a professional development. Great Britain follows close with nearly 22% from 2022 to 2025. Italy saw plus 15% at the same time but still has many small PCB manufacturers and lost 2 last year. Central and Eastern Europe, like Germany, saw a three-year consecutive decline of 12.5% against 2022. This is due to a strong decline from 47 to 33 companies, mainly small manufacturers.

Whereas bigger companies can focus on a specific market segment (e.g. Air, Space & Defense) or technologies (e.g. HDI or flex and rigid-flexible ML and/or HDI), smaller companies often lack technological capabilities and/or market reputation and thus fight a daily price fight against competition from Far East. No wonder, Data4PCB expects the number of European PCB manufacturers to reduce by half by 2035, if the European Union does not lift the unfair import duties on base materials for European PCB manufacturers while allowing finished PCBs from Far East to be imported without tariffs.

Another important step towards European independence would be to define a secure supply chain for system-critical products in Europe, using European-made PCBs.

The full report is available by contacting [email protected]