Dr. Mareike Haass & Michael Künsebeck, in4ma

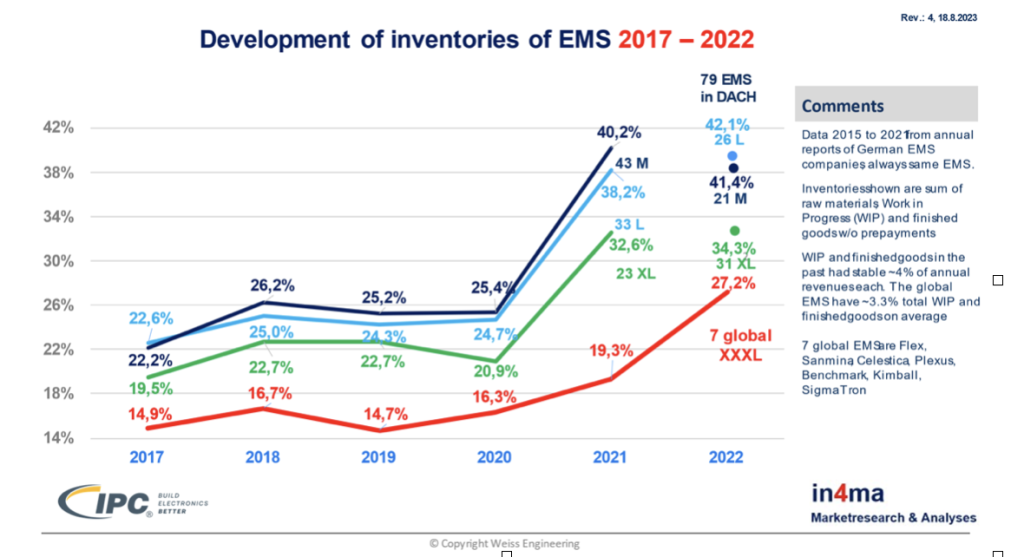

For nearly two years the electronics industry has experienced a shortage of semiconductors. In response, electronics manufacturers built up huge amounts of inventory as a preventive measure. Tracking this as a percentage of revenues and assuming 2017 to 2020 to be the norm, inventories increased by 60 to 80% in 2022.

In Europe for smaller companies with lower revenues, this percentage was even higher. Why? Because small companies generate their revenues primarily by PCBA manufacturing only, whereas the bigger players have additional added value with box-building and other related services that have higher margins. Comparing the European numbers with seven global EMS companies reveals they are even lower, in normal times as well as during the “chip crisis”. This is because the big global players generate even less revenue from the assembly of PCBs. Sanmina, Kimball and Flex manufacture PCBs but have diversified manufacturing services; at Jabil, diversified manufacturing services are as high as 50% of their revenues, resulting in Jabil’s inventory build-up in 2022 only reaching to 14.7% of revenues.

The major share of inventories is always raw materials, and this can be tracked for the public EMS companies from their annual reports. We left Jabil out of this evaluation to avoid skewing the results.

At the end of 2022 the electronics industry was sitting on huge piles of inventories and the question arises, if this was all material badly needed due to the crisis, would it not have been possible to use it and get inventories down again fast?

Now it is the middle of 2023, and the first three global companies, Flex, Kimball and SigmaTron already published their fiscal year 2023 results. Surprisingly, all three companies had a further build-up of inventories in absolute terms, increasing by 14.1%. At the same time, they increased their revenues on average by 17.3%. This does not look as if these companies were focused on reducing inventories.

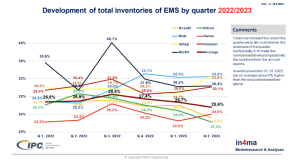

We then looked at the last six quarterly results of seven public EMS in Europe (Scanfil, Kitron, Note, Hanza, InCap, Inission and Norbit).

In absolute terms, their total inventories increased by 15.1% end of Q 1. 2022; 10.1% by Q 2. 2022; 7.2% by Q 3. 2022; 4.4% by Q 4. 2022; minus 0.2% by Q 1, 2023; and minus 2.0% by Q 2. 2022.

These seven European EMS increased their revenues in 2022 by a stunning 40.5% but still increased their inventories on an annualized basis from 29.6% to 29.9%. In the quarterly calculation shown above we were able to see a slight reduction on a percentage base on the first two quarters of 2023, but the reduction in absolute terms was marginal.

This raises the question, whether the companies are still holding on to these high levels of inventory to be better prepared for future crises or whether it is the rigid NCNR (non-cancellable, non-returnable) policy of the distributors preventing a further reduction.

We are at present in a phase of high interest rates, which is going to last several years according to the economists. Cash is king in such times and inventories are still binding too much cash. The aforementioned seven global EMS alone are holding about 1.38 billion USD in excessive inventory (if one takes the inventory percentage of 2019 as the norm, multiply this with the revenues of YE 2022 and compare this with the actual inventories YE 2022).

The situation in general is more than unhealthy and requires the full attention of the EMS companies as well as talking with distributors and manufacturers to find a suitable solution which allows everybody to achieve a reasonable result.

This is even more pressing, when looking at the revenue development of the seven public European EMS. Quarter to quarter their revenue increase was 2.5% in Q 1. 2023 and 2.1% in Q 2 2023. Compared to the first half of 2022, the first half 2023 saw a growth of 19.1%, which is in line with the in4ma half year survey we are currently preparing. But the tremendous growth rates will not continue. Several OEMs are already trying to defer deliveries as their warehouses are full.