October–December

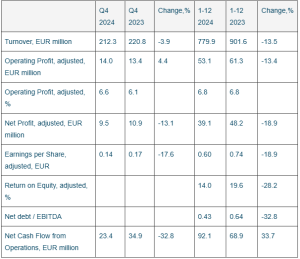

• Turnover totaled EUR 212.3 million (220.8), a decrease of 3.9%

• Adjusted operating profit was EUR 14.0 (13.4) million, an increase of 4.4 %. Reported operating profit was EUR 13.8 (13.4) million, an increase of 2.9 %

• Adjusted 0perating profit margin was 6.6% (6.1%). Reported 0perating profit margin was 6.5% (6.1%)

• Earnings per share were EUR 0.14 (0.17)

January–December

• Turnover totaled EUR 779.9 million (901.6), a decrease of 13.5%

• Adjusted operating profit was EUR 53.1 (61.3) million, a decrease of 13.4%. Reported operating profit was EUR 52.6 (61.3) million, a decrease of 14.2%

• Adjusted operating profit margin was at 6.8% (6.8%). Reported operating profit margin was at 6.7% (6.8%)

• Earnings per share were EUR 0.59 (0.74)

• Net debt/EBITDA was 0.43 (0.64)

• Dividend proposal 0.24 (0.23) euro per share

Outlook for 2025

Scanfil estimates its turnover to be EUR 780-920 million and operating profit EUR 53-66 million in 2025.

Adjusted items are non-recurring significant items that deviate from normal business operations, which affects the comparability between different periods. Adjusted items in January-September include costs related to the acquisition of SRXGlobal Pty Ltd. (EUR 0.3 million).

CEO Christophe Sut:

“The fourth quarter was the best quarter of the year, and we delivered an adjusted operating profit of EUR 14 million. In absolute terms, the improvement was EUR 0.6 million compared to the same period last year. The adjusted operating margin was 6.6%, an increase of 0.5 percentage points from last year.

The fourth quarter closed a full year where Scanfil demonstrated an ability to defend its operating margin and maintain a solid 6.8% adjusted operating margin in a challenging market situation. Excluding full-year impacts of foreign exchange rates, layoff costs, and material consignment sales, the full-year operating margin reached our long-term target of 7.0% and demonstrated great operational performance throughout the year.

At the end of the fourth quarter, our financial position was solid. Gearing was 7.3% (19.4%), and the equity ratio was 55.5% (53.7%). Inventory management improved, and inventories were reduced by EUR 5.8 million in the fourth quarter. Compared to the end of December last year inventories decreased by EUR 51.4 million (Cash flow impact of inventory reduction). Our net debt level was 0.43 times EBITDA, well below our long-term target of 1.5.

The Board of Directors’ dividend proposal per share is EUR 0.24, which is 41% of the earnings per share. We aim to pay our shareholders an increasing dividend and keep our balance sheet strong to be able to carry out all strategically important growth investments. If the Annual General Meeting approves the proposal, the dividend has increased for 12 consecutive years.

On the customer side, we continued to focus on winning new contracts and had another very active quarter in sales, winning new projects with a record annualized value of EUR 61.0 million in the fourth quarter and EUR 187.5 million in 2024.

The Industrial segment remained slightly negative compared to last year, with turnover decreasing by 5.0%. The market was soft, and volumes stabilized at a lower level. However, our new sales activity was strong, and we won new projects with an annualized value of EUR 31.6 million in the fourth quarter and EUR 83.2 million in 2024.

The Energy & Cleantech segment stabilized at lower levels. Turnover development was -7.8% for the fourth quarter and -13.9% for the full year compared to the same period in 2023. The long-term outlook remains positive, and we won projects in the fourth quarter with an annualized value of EUR 19.9 million and EUR 73.7 million in 2024.

The Medtech & Life Science segment developed positively in the second half of 2024 and returned to growth. Turnover increased by 7.6% in the fourth quarter, but the full-year turnover development was still slightly negative at 5.1% compared to 2023. Investments in sales resources started to pay off, and we signed several new contracts. In the fourth quarter, the annualized value was EUR 9.5 million and EUR 30.2 million in 2024.

The strategic changes announced during the third quarter are now fully implemented. At the beginning of 2025, our new regional operating model and supporting Management Team were fully operational.

The SRXGlobal acquisition was completed early in the quarter, and we focused on integrating and leveraging the newly acquired assets. Anticipating strong customer demand and a promising long-term outlook, we have decided to invest EUR 4.3 million in the Malaysian factory. Our financial position will allow us to continue to look for new M&A opportunities.

We see customer demand stabilizing and rebounding; this was the case with Medtech & Life Science. We believe demand will gradually speed up in 2025, and in the first quarter of the year, we will focus on ramping up customer projects won in 2024. Our outlook for 2025 in turnover is EUR 780–920 million and an operating profit EUR 53-66 million. The first quarter of 2025 is a ramp-up quarter of projects we won in 2024. It builds-up a momentum for a brisk remainder of the year.

In 2024 our team has shown strong commitment to implementing the strategy and reaching our targets in a challenging market situation. We are building our strength through efficiency improvements, new customer contracts, and M&A”.

Turnover

The turnover for October–December was EUR 212.3 (220.8) million, a decrease of 3.9% compared to the previous year’s comparison period. The revenue included EUR 14.5 million of material sales to consignment inventory with low margin. The turnover decreased by EUR 8.6 million, of which EUR 2.4 million were spot market purchases. Excluding spot market purchases impact, turnover decreased by 2.9%.

The turnover for January–December was EUR 779.9 (901.6) million, a decrease of 13.5% compared to the previous year. The turnover decreased by EUR 121.7 million, of which EUR 14.5 million were spot market purchases. Excluding spot market purchases, turnover decreased by 12.1%.

In January–December, the largest customer accounted for about 13% (13%) of turnover and the top ten customers accounted for about 55% (55%) of turnover.

Turnover by customer segment

Industrial

Turnover in October–December was EUR 99.9 (105.2) million, a decrease of 5.0% compared to the same period in 2023. Turnover in January–December was EUR 368.3 (427.6) million, a decrease of 13.9% compared to 2023. The general economic situation had a negative impact on certain end-customers’ demand.

Energy & Cleantech

Turnover in October–December was EUR 72.4 (78.5) million, a decrease of 7.8% compared to the same period in 2023, which was caused by cyclic demand variation with certain customers. Turnover in January–December was EUR 265.8 (320.2) million, a decrease of 17.0% compared to 2023. Improved semiconductor availability in the second half of 2023 boosted the demand and drove to overstock, which impacted the turnover.

Medtech & Life Science

Turnover in October–December was EUR 40.0 (37.1) million, an increase of 7.6% compared to the same period in 2023. The increase resulted from a positive development with certain end customer demand. Turnover in January–December was EUR 145.8 (153.7) million, a decrease of 5.1% compared to 2023. The decrease was mainly caused by a strong comparison period in 2023.

Operating profit

The adjusted operating profit for October–December was EUR 14.0 (13.4) million. With a strong focus on reducing operational costs, the operating profit increased by EUR 0.6 million from the previous year, and the adjusted operating margin improved to 6.6% (6,1%) of turnover. The adjusted operating margin was impacted by an EUR 0.4 million negative change in foreign exchange rates and EUR 14.5 million in consignment sales, resulting in a 0.7% negative impact on the operating margin. Operating profit was adjusted with EUR 0.2 million acquisition costs related to SRX transaction in the fourth quarter of 2024. The operating profit for October–December was EUR 13.8 (13.4) million, 6.5% (6.1%) of turnover.

The adjusted operating profit for January–December was EUR 53.1 (61.3) million, 6.8% (6.8%) of turnover. Operating profit was adjusted for EUR 0.5 million acquisition costs related to the SRX transaction. The adjusted operating margin was affected by EUR 1.0 million change in foreign exchange rates, EUR 0.5 million in lay-off costs, and EUR 14.5 million in consignment revenue, resulting in a total impact of -0.3%. The operating profit for January–December was EUR 52.6 (61.3) million, 6.7% (6.8%) of turnover.

Net profit and earnings

The net profit for October–December was EUR 9.2 (10.9) million, a decrease of 15.0%. Earnings per share were EUR 0.14 (0.17). The net profit for January–December was EUR 38.6 (48.2) million, a decrease of 19.9%. Earnings per share were EUR 0.59 (0.74). The return on investment was 15.4% (19.4%).

The effective tax rate in January–December was 24.4% (21.7%). The difference in the rates is due to a negative adjustment of taxes in the Poland Special Economic Zone and a tax refund resulting from a mutual agreement process in 2023 concerning the 2014 tax year in Poland. These factors had a total impact of 1.4% on the tax rate. Otherwise, the tax rate reflects the weighted average tax rates, including withholding taxes on dividends.