Amid deepening geopolitical fragmentation, the United States imports $3 trillion in manufactured goods annually. About 25 percent of these are particular “Achilles’ heels”—due to some combination of criticality to national security, supply concentration, and geopolitical distance from trade partners. About 5 percent of manufacturing imports—overwhelmingly computers and electronic products—have all three dependencies.

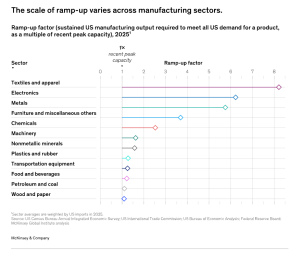

McKinsey’s new report, ‘Ramping up manufacturing in America?’ introduces a “ramp-up factor” to quantify what it would take for the United States to produce more at home. For those exposed products in the Achilles’ heel, manufacturing would need to double on average to fully meet domestic demand. In some cases the ramp-up factor is much larger, for example, over five for some active pharmaceutical ingredients and over ten for AI servers. Across all products, the number is smaller: 1.3.

Running today’s factories at peak capacity would generate $660 billion more in output—but hardly touch the biggest exposures. About 40 percent of this extra production would be in transport equipment and another 40 percent from metals, wood and paper, chemicals, and plastic and rubber.

Addressing key vulnerabilities would require a transformed industrial base. Building capacity to produce exposed products and their upstream inputs could cost on the order of $2 trillion, about 6 percent of GDP. Funding could be the (relatively) easy part: Specialized skills, supporting infrastructure, sufficient energy, and shovel-ready projects are all needed.

Nothing will happen without a business case. Maintaining competitiveness in the global economy, and security in a volatile world, may require some domestic ramp-up. But this will entail prioritization and trade-offs, along with new approaches to technology, automation, and skills.

“Made in America” has been part economic policy and part rallying cry for generations. But the United States has been producing less and less of the global total. In 2000, it was the world’s leading manufacturer. Today, the country produces just a quarter of China’s output. The United States did not lose manufacturing dominance overnight, and it remains the world’s second-largest producer. As the global economy grew, trade liberalization, modern shipping containers, and global internet connections unleashed potential for a “great unbundling.” Lower-cost emerging economies took on physical production of many goods, while the United States provided much of the technology and manufacturing know-how.

Should the United States attempt to rebuild its industrial base? For decades, proponents have pointed to the widening trade deficit and shrinking manufacturing base as drags on US growth that drain the economy’s ability to create high-paying jobs. Others counter that the economy operates most efficiently when businesses and consumers can buy the goods and services they want at the highest quality and for the lowest price, wherever they come from, and that the trade deficit arises more from US savings and investment dynamics than from trade policies.

Today’s age of increasing geopolitical competition and rapid technological progress has recast the debate with renewed intensity. Simply assembling goods in the United States may not be enough to alleviate concerns about the manufacturing sector. The materials and components that go into AI technology, smartphones, and electric vehicles are just as crucial. Both economic and national security may hinge on reliable supply chains. For things like ships and chips, the United States may decide it cannot be beholden to others.

It’s not just about limiting risk. In some advanced industries, the rapid innovation that drives national competitiveness and productivity growth increasingly depends on maintaining a close connection with physical production, even where software and design once seemed to be decoupled from manufacturing. For example, like humans, industrial robots driven by AI learn and adapt fastest when they get real-time feedback from the physical world, not delayed, batched input.

For all the current attention, there is limited nuts-and-bolts understanding of what achieving these broad objectives would entail. A great deal of analysis has focused on specific industries critical to national security, including semiconductors, quantum computers, pharmaceuticals, and defense. It gets at important details but is narrow in focus. Another strand of macro-level inquiry looks at factors like balance of trade, labor statistics, and the relative productivity of manufacturing compared to service industries. It is broad but not detailed enough to cast light on specific areas of potential or to quantify trade-offs between efficiency, innovation, jobs, and security.

No matter what, ramping up broad swaths of US manufacturing may seem a daunting prospect. A number of factors would need to be considered. Many thousands of new factories would need to be built. Workers with the right specific skills would need to be available at the right time and in the right places. All of this would require funding, and that would in turn depend on compelling and concrete business rationales—the more expensive the project, the bigger the potential for payoff—and would need to be considered in the context of the policy and regulatory environment. And the transformation would require coordinated shifts of all of these ecosystems across entire supply networks.

But just how daunting is it? Answering that requires first understanding, product by product, the scale of the US production ramp-up needed to fully meet domestic demand. Ultimately, macro-level assessments of necessary labor, funding, sequencing, and timelines hinge on this micro-level data.

This report aims to provide that foundation, focused specifically on the question of existing and needed future capacity, as a critical input for policymakers and business leaders to systematically decide whether and where to prioritize domestic manufacturing efforts.