Background and Purpose

The accelerating trend of reshoring to achieve a regional strategy has brought EMS business back to North America. EMS companies are expanding capacity in this region and OEMs are looking for manufacturing partners as they execute these plans. The EMS industry is rapidly changing in terms of types and range of services provided, profitable capacity, reputation, technological capabilities, supply chain management and engineering skills, types of products being built and overall financial health from revenue diversification – historically a hard nut to crack. The need to expand the capacity and capabilities, including rebuilding the semiconductor and other component ecosystem means the industry needs to substantially grow to accommodate the rising expectations of consumer and industrial customers alike.

A second trend impacting the NA EMS industry is the expansion of electronic technology into non-traditional areas such as smart homes, agriculture, e-vehicles, patient monitoring, wearables, and so on seemingly into every aspect of life. This expanding total market requires more hardware engineering and manufacturing capacity.

In response to these trends, EMSNOW is compiling data and company profiles to help OEMs identify EMS companies that have the capabilities and experience to provide required services in North America. We have been covering this industry for decades and we do not believe that anyone has a solid handle on how many EMS companies actually are in operation in North America. There are directories, but the devil is in the details. This industry is in a constant state of flux. More visibility is needed to help OEMs connect with EMS partners. As has always been the case, the key to finding the right EMS requires careful alignment of a particular OEM’s requirements with compatible EMS’ capabilities.

Our goal is to provide an operational profile of the EMS industry in North America based on primary survey data and secondary research. We identify EMS companies of all sizes that can provide services and we track trends that can help guide the OEM. All these resources can be accessed through EMSNOW.com.

EMSNOW is not a market research firm, nor do we aspire to become one, but we recognize the need for better market research on the EMS industry in North America. We appreciate the example that in4ma has set for EMS industry research in Europe and see it as a model of what is needed for North America. Dieter Weiss and his team compile information about the EMS industry in startling detail and granularity based on painstaking primary and secondary research. In4ma has gained the trust of the industry with support and cooperation from companies of all sizes, public and private. They report all data in aggregate, revealing nothing proprietary, and the wide industry participation rate is good for everybody. Here is an excerpt from their website:

In three years of work, Weiss Engineering identified more than 2160 EMS companies in Europe, as well as about 70 EMS companies in the Middle East, Israel and the Maghreb countries. In addition to contact details, sales and employee numbers, and (in some cases) other figures from the balance sheet and income statement were recorded. Revenues were recorded retroactively up to 2013, balance sheet data retroactively to 2014. The source was both country-specific company registers and paid databases. This enabled more than 85% of the European production volume to be directly tracked. SOURCE: in4ma website

EMSNOW’s research efforts via this second annual EMS industry survey for EMS in North America is an attempt to help fill the research void. In order to capture the benefit of the expected investment flooding electronics manufacturing from recent legislation, as well as the renewed interest in regional manufacturing footprints, the industry needs more visibility.

We thank the companies that participated in the survey. Those that agreed to be listed are in the chart at the end of this report.

Methodology

This, the second annual survey of North American EMS companies, was conducted with the same methodology as the first. Survey data was collected via SurveyMonkey online, by casting a wide net via email request to several email lists including EMSNOW’s Daily Newsletter, IPC membership lists, and LinkedIn groups.

The qualifier to complete the survey this year was the same as well: the participant company must provide PCBA as a core service to be considered an EMS company for the purposes of this research. Participants also needed to have facilities operating in North America.

The survey was open October 2022 through March 2023; in that time a total of 67 EMS companies completed the survey. Numerous companies were removed from analysis due to duplication, or not having North American based operations.

The data in the charts represents only the responses of the 67 who completed this survey; we believe this is representative of the broader EMS industry in North America based on our past research and experience tracking the EMS industry for nearly 30 years.

Of the 50 companies on the MMI Top 50 Global EMS, eight of them are based in North America. Our survey respondent pool included representative Tier 1 and Tier 2 companies from this list with facilities in North America.

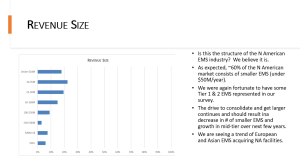

Our data from this group of respondents points to the fact that approximately 60% of the North American market comprises smaller EMS (under $50M revenue). The drive to consolidate and get larger continues and should result in a decrease in the number of smaller EMS and growth in mid-tier over the next few years.

Changes to Survey in 2022

Several changes were made to this year’s survey. At the request of IPC, employee base was changed to a tiered selection, rather than absolute numbers. The $10-50M revenue category was divided into two categories of $10-25M and $25-50M.

The questions related to size and composition of customer base were replaced by a question about the % of revenue generated by EMS business.

EMSNOW North American EMS Industry Survey Results: 2022 Findings

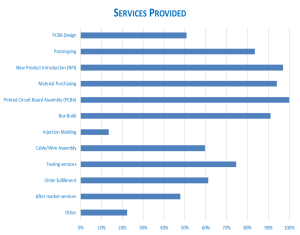

Services Provided

For this survey section, PCBA was the qualifier for inclusion in the study. All EMS provided a full suite of services; NPI, material purchasing, box build, and prototyping were all cited by over 80% of respondents.

Interestingly, the ‘other’ category included mostly items that could be included in provided categories, but also this year included metal fabrication and conformal coating. Several companies listed items that would be considered ‘after market services’. Adding to the list of services continues to be a way for EMS companies to differentiate themselves and avoid becoming a commodity.

Operations Overview

The next few charts pertain to respondents operational footprint, including manufacturing facilities in North America, SMT lines, and manufacturing floor space in square feet.

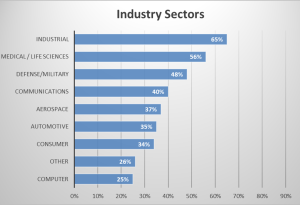

End Markets Served

The survey data show that end markets served has expanded dramatically as electronics are added to an ever-increasing number of products. EMS companies are finding their customers in non-traditional end markets.

This data also reflect the higher mix, low to medium volume manufacturing work most common in North America. About a third of the respondents included manufacturing in sectors other than the traditional ones we listed. This speaks to a couple issues: Companies are attempting to differentiate themselves in more specialized fields. Subsectors of the “Industrial” sector, which has always been the most general of the traditional sectors, are growing and becoming credible industry sectors in their own right.

This year the ‘other’ category included, in order of most to least mentions:

- Semiconductor equipment

- Test and measurement (formerly called ‘instrumentation’)

- Lighting

- Agriculture

- Electrification/EV/charging stations

- Energy

- Mining, oil exploration

- Gaming

- Robotics

- Biotech

These sectors have historically been included in other sectors such as Industrial and Medical, but this may be changing as these areas advance and differentiate. For example, while the ‘Communications’ sector historically meant cell phones, it is clear that today it includes a wider range of RF systems that are used in regulated industries and are produced in lower volumes. Hence the high percentage of North American EMS companies citing that industry sector in their customer mix than would be expected. High volume cell phone production has not been in the North American EMS portfolio for many years.

Revenue Size and Non-EMS Revenue

Non-EMS Revenue

- Of the 67 respondents, only 45 stated that 100% of their revenues came from their EMS services.

- The other 22 respondents stated a range for their EMS generated revenues of 15% to 99%

- Many of the “other revenue generating” services they reported could in fact be considered EMS services.

- However, these activities received the most mentions:

- OEM product line (4)

- PCB fab (1)

- Component sales (1)

- Training (1)

- Photochemical etching (1)

- EMI/RFI stamping (1)

- We conclude that these are examples of the EMS strategy of revenue diversification that has been adopted over the years by many EMS large and small.

Conclusion

We offer these survey results to point the way to further research that must be done to prepare for the growth expected in the coming years. The EMS industry in North America must become more visible to the OEM communities looking for regional manufacturing partners. These are not traditional OEMs from the ‘3 C’s’ of a few decades ago: communications, computing, consumer. As our survey has shown that ‘other’ category is where all the growth will occur. It is also where the next generation of OEM engineers are developing the latest product ideas. They are looking for true partners to bring these ideas to reality. Electronics manufacturing is no longer in danger of becoming ‘commoditized’ where price is the only factor. These complex products being used in new environments and applications will require sophisticated design and engineering support throughout the product development cycle. For products in regulated industries and increasingly to meet environmental sustainability goals, OEMs will be relying on their EMS partners to stay on top of all the legislation. These are positive trends that bode well for this industry. We intend to continue to bring attention and visibility to help EMS companies connect with appropriate customers.

Again, we thank the companies that participated. Those that agreed to be listed are in the following chart.