Outlook According to ECIA’s Industry Pulse: Electronic Component Trends and Sentiment October 2025

By Dale Ford, Chief Analyst, ECIA

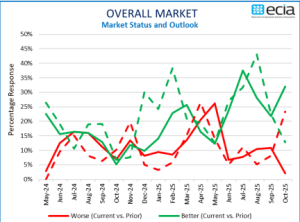

The results of the October Industry Pulse survey reveal that overall sales sentiment was sustained at a strong level in October with an overall index average of 122.2, an increase of 4 points from September. However, the overall sentiment looking forward to November collapses by 18.7 points, down to 103.5, according to survey results.

The results of the October Industry Pulse survey reveal that overall sales sentiment was sustained at a strong level in October with an overall index average of 122.2, an increase of 4 points from September. However, the overall sentiment looking forward to November collapses by 18.7 points, down to 103.5, according to survey results.

While a slowdown in month-to-month expectations for sales growth as we approach the end of the year is not surprising, the steep decline in the index average is startling. The precipitous decline in sales sentiment for Passive Components is shocking as the index collapses by 26.3 points down to 93.8. Inductors and Capacitors are the primary culprits in the demise of Passive Component sales sentiment looking toward November.

Fortunately, the Electro-Mechanical Components and Semiconductor survey results for the November outlook registered above the 100- point threshold for expected sales growth. The drop in sales sentiment for Electro-Mechanical components was as steep as the drop for Passives. However, the stronger October sentiment yielded an index score above 100 for November despite the 24.5-point drop.

The most stable component category in the survey was Semiconductors. It saw an increase of 5.2 points between September and October. The November outlook simply erased this improvement as Semiconductor sentiment dropped back to the September level of 105.9.

The Industry Pulse sees the market slamming on the brakes as we approach the end of 2025. The end-market index results for October and November are breathtaking as the index soared by nearly 19 points between September and October, only to tumble like Icarus, flying too close to the sun, as the November score careened down by 40 points to 89.4.

While all eight individual end-market segments achieved sales sentiment scores at or above 100 in October, only four were able to sustain sentiment above 100 in the November projections. Automotive and Medical Electronics took the hardest hits in the November forecast.

While all eight individual end-market segments achieved sales sentiment scores at or above 100 in October, only four were able to sustain sentiment above 100 in the November projections. Automotive and Medical Electronics took the hardest hits in the November forecast.

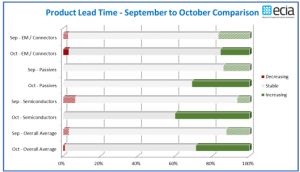

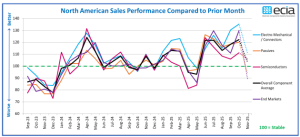

Beginning with the April survey, ECIA began measuring sales sentiment compared to the same month in the prior year. From this perspective, both the product and end-market sentiment show impressive strength compared to the prior year throughout the survey period of April to October. Every segment shows exceptionally strong sales sentiment improvement year-over-year. For many months, the Industry Pulse survey results for product lead times have reflected great stability with almost no reports of increasing or decreasing lead times. This changed abruptly with the reported lead time trends for October.

Reports of increasing lead times by survey participants for Semiconductors leapt from 7% in September to 40% in October. There were no reports of decreasing lead times for Semiconductors in October. Passives also saw a major jump in lead times between September and October with the number of survey participants reporting increases growing from 14% to 31%. ElectroMechanical Components lead time reports remained stable at around 16%. The lead time results for October are consistent with the many months of strong sales sentiment through October. It may be that the softness in sales sentiment in November will also relieve pressure on lead times.

The ECST survey provides highly valuable and detailed visibility on industry expectations in the near term through the monthly and quarterly surveys. This “immediate” perspective is helpful to participants up and down the electronics components supply chain. In the long-term, ECIA shares in the optimism for the future as the continued introduction and market adoption of exciting innovative technologies should motivate both corporate and consumer demand for next-generation products over the long term.

The complete ECIA Electronic Component Sales Trends (ECST) Report is delivered to all ECIA members as well as others who participate in the survey. All participants in the electronics component supply chain are invited and encouraged to participate in the report so they can see the highly valuable insights provided by the ECST report. The return on a small investment of time is enormous!

The monthly and quarterly ECST reports present data in detailed tables and figures with multiple perspectives and covering current sales expectations, sales outlook, product cancellations, product decommits and product lead times. The data is presented at a detailed level for six major electronic component categories, six semiconductor subcategories and eight end markets. Also, survey results are segmented by aggregated responses from manufacturers, distributors, and manufacturer representatives.