- China’s smartphone shipments declined 1.6% YoY in Q4 2025 and 0.6% YoY for the full year, primarily due to weak demand caused by rising prices resulting from memory shortages.

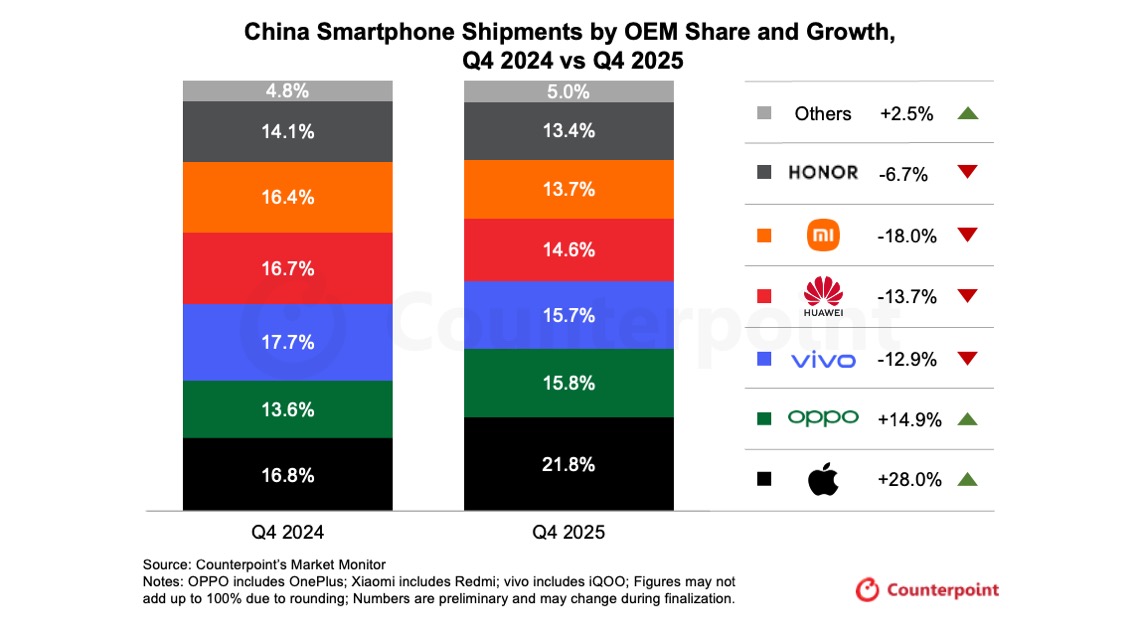

- In Q4, Apple’s shipments rose 28% YoY and led the Chinese smartphone market, driven by strong traction for the iPhone 17 series.

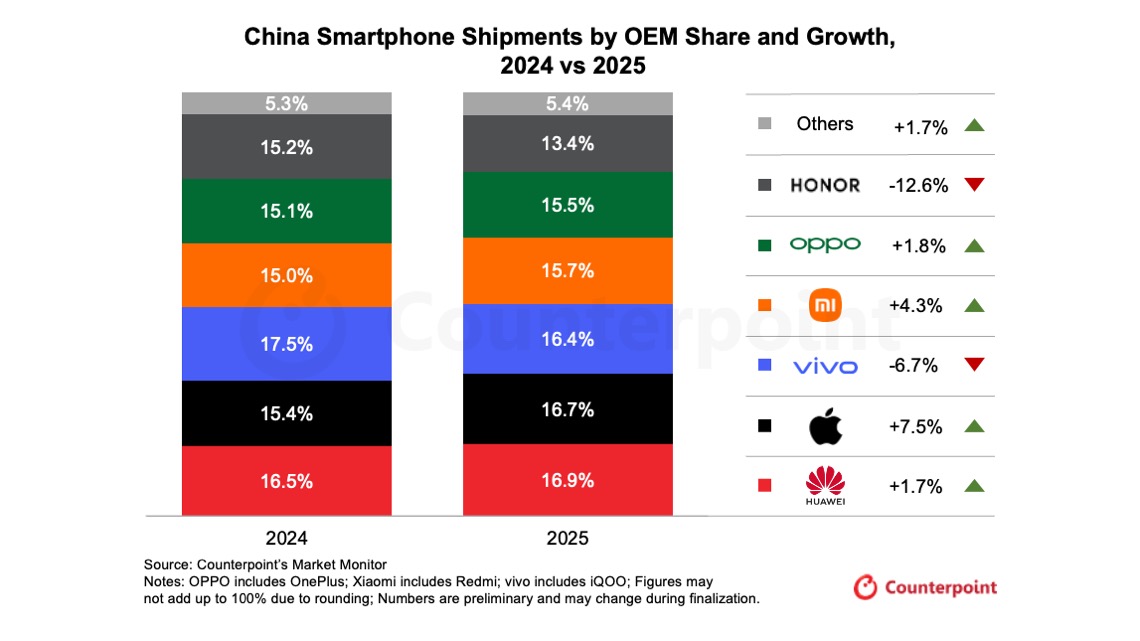

- For full-year shipments, Huawei ranked first on strong performance in the first half of the year, supported by solid mid-to-high-end performance after price adjustments and government subsidies.

- Faced with rising memory costs, smartphone OEMs have scaled back certain low-end product lines. The market’s downward trend is expected to further deepen in the coming year.

Beijing, Berlin, Buenos Aires, Fort Collins, Hong Kong, London, New Delhi, Seoul, Taipei, Tokyo – China’s smartphone shipments fell 1.6% YoY in Q4 2025 and 0.6% YoY for the full year, according to preliminary data from Counterpoint Research’s Market Monitor Tracker. Apart from Q1, when government subsidies provided a temporary uplift, shipments in all other quarters of 2025 recorded YoY contractions.

Apple led China’s smartphone market in Q4 with a 22% share, driven by strong traction for the iPhone 17 series and an accelerated supply ramp. The Pro series, with its distinctive new camera design, and the base variants, with double the storage of last year’s equivalent but at the same price, have all seen a strong market response. Sales for the iPhone Air, which saw a delayed launch, came in at a low single-digit share. Senior Analyst Ivan Lam said, “The late launch and trade-offs between thinness and the feature set resulted in a slow start for the iPhone Air. But it’s a significant product, not only as an exploration into ultra-thin design, but also when considering the longer-term structural implications for the domestic market for eSIM smartphones.”

OPPO moved up to second place in Q4 on 15% YoY growth, driven by sustained strong demand for the Reno series, alongside incremental volumes contributed by the newly launched Find X9 and OnePlus 15 series.

Huawei ranked first in the Chinese market for the full year, despite experiencing a YoY decline in the second half of the year. Huawei’s mid-to-high-end models performed strongly following price discounts, reinforcing its overall market leadership. The delayed launch of the Huawei Mate 80 series relative to competing models weighed on its Q4 performance. However, we observed a strong rebound at the start of 2026, supported by a new round of subsidies.

Despite YoY declines in Q4, vivo, Xiaomi and HONOR showed some positive highlights. The vivo iQOO 15 delivered exceptional value for money among devices powered by Qualcomm’s latest flagship chipset. The Xiaomi 17 series saw early-quarter momentum, with its Pro models’ innovative rear display being a standout. The Xiaomi 17 Ultra launched two months earlier than its predecessor, underscoring an accelerated flagship cadence to secure first-mover advantage. HONOR’s X70 and 400 series maintained solid demand, while the newly released WIN series drew attention for its thermal performance.

Looking ahead, according to Counterpoint’s Memory Tracker and Forecast Insights Report, memory prices are expected to rise further, by 40%-50% in Q1 2026, followed by an additional increase of around 20% in Q2 2026. Amid rising memory costs, smartphone OEMs are expected to optimize their product portfolios, with a particular focus on scaling back low-end models to preserve margins. The new round of national subsidies has partially alleviated cost pressures across the industry. However, we remain cautious on the overall smartphone market outlook for this year.