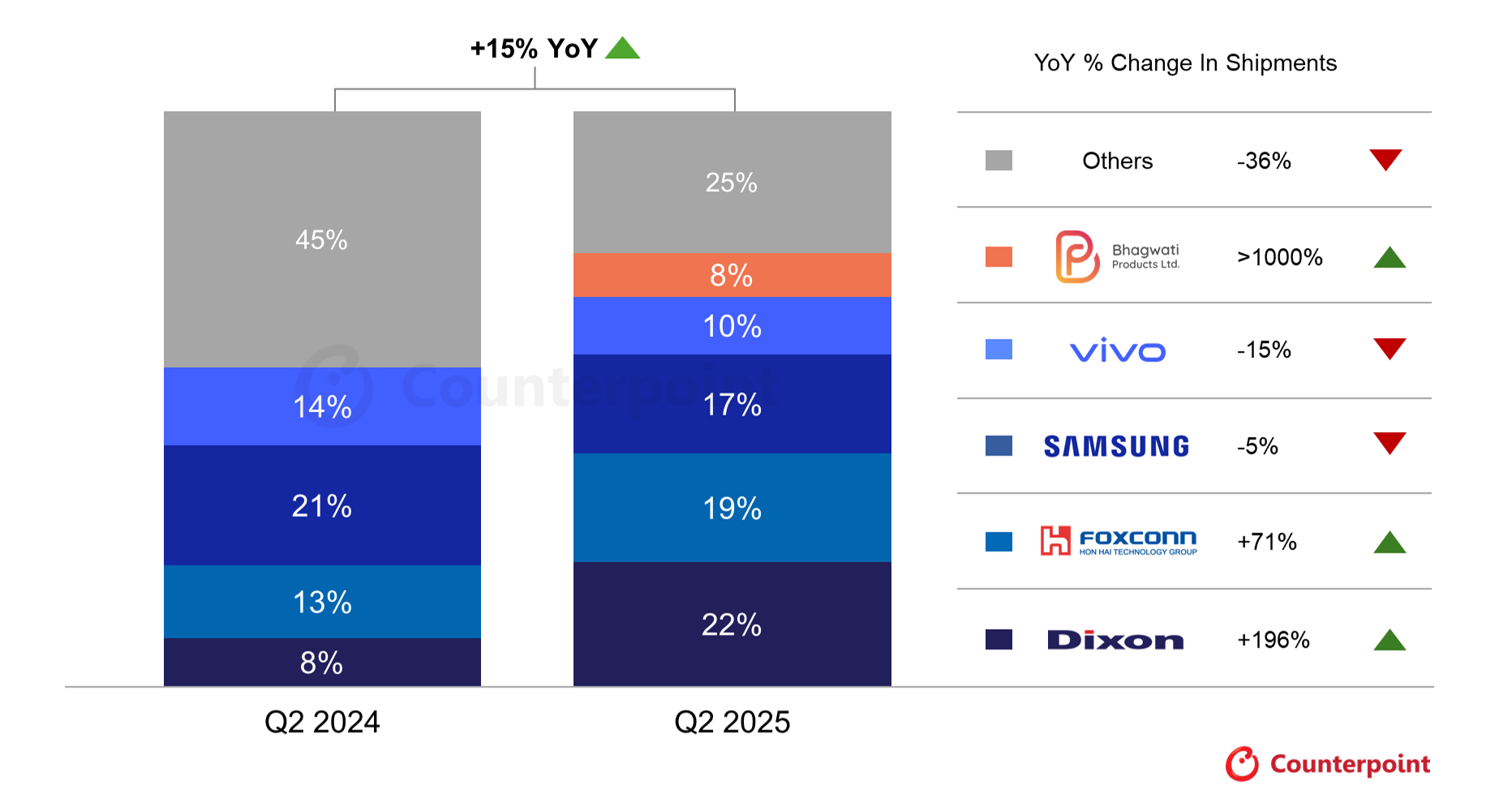

- ‘Made in India’ smartphone shipments grew 15% YoY in Q2 2025, driven by a 32% surge in exports and an 8% rise in domestic sell-in.

- Dixon Technologies became the top smartphone manufacturer by shipments for the first time, recording 196% YoY growth, driven by rising orders from Motorola, Transsion brands, Xiaomi and realme.

- Foxconn Hon Hai captured the second spot, registering 71% growth due to a surge in iPhone exports.

- Bhagwati Products Limited entered the list of India’s top five smartphone manufacturers for the first time as an EMS player. It also became the fastest-growing manufacturer, driven by an uptick in vivo and OPPO orders.

Shipments of ‘Made in India’ smartphones grew 15% YoY in Q2 2025, driven by a 32% surge in exports and an 8% rise in domestic sell-in, according to Counterpoint Research’s ‘Make in India’ Tracker. Dixon Technologies* grew by 196% YoY to become India’s largest smartphone manufacturer for the first time. The company was in sixth place in Q2 2024. Dixon’s growth was driven by rising orders from Motorola, Transsion brands, Xiaomi and realme.

With its production crossing 2 million units per month, driven by orders from vivo and OPPO, Bhagwati Products Limited (BPL) recorded the fastest growth in the market and jumped into the top five for the first time. Foxconn Hon Hai and Tata also grew, driven by increased exports and domestic demand for iPhones.

Commenting on the manufacturers, Senior Research Analyst Prachir Singh said, “Indian manufacturers are now playing an important role as major Chinese OEMs have outsourced their production to these local players. Going forward, we expect the EMS* (electronics manufacturing services) landscape to expand in India, with local manufacturers benefiting. The government has also launched the Electronics Component Manufacturing Scheme that will play a key role in the expansion of the country’s electronics manufacturing supply chain. Technology partnerships with important global ODMs (original design manufacturers) and component manufacturers will be a key element for electronics manufacturing growth in India.”

India Smartphone Shipment Share by EMS, Q2 2025 vs Q2 2024

Source: Counterpoint’s ‘Make in India’ Service Note: Percentages may not add up to 100% due to rounding.

Commenting on the growth in exports, Research Analyst Tanvi Sharma said, “Apple was the largest exporter in Q2. Geopolitical maneuvering owing to Trump’s tariffs opened the way for India to become a more attractive destination for sourcing smartphones, leading to a surge in exports, especially for iPhones. This benefited Foxconn Hon Hai and Tata Electronics. Exports for Motorola also grew, driven by a rise in demand in the US, which benefited Dixon.”

Commenting further, Research Associate Abdul Rehman said, “Apple and Samsung led the export market with a consistent combined share of more than 93% of Made in India smartphones. While short-term global disruptions have helped EMS players based in India to boost outward shipments, long-term sustenance of exports is contingent upon anchoring India as a key player in the global supply chain. This is possible only through deeper investments towards building a robust ecosystem for smartphone components in India.”

The role of Indian manufacturers is expected to expand in the coming months. BPL is ramping up production, while Dixon has announced a joint venture with India’s top smartphone player vivo. Many such manufacturers have also invested in developing a component ecosystem in India through joint ventures for displays, camera modules, mechanics and more, which will further increase the domestic value addition in India.

*Notes: Dixon Technologies includes Padget; EMS here means “in-house design + EMS manufacturing” orders

About Counterpoint Research

Counterpoint Research is a global market research firm specializing in products across the technology ecosystem. We advise a diverse range of clients – from smartphone OEMs to chipmakers and channel players to Big Tech – through our offices located in the world’s major innovation hubs, manufacturing clusters and commercial centers. Our analyst team, led by seasoned experts, engages with stakeholders across the enterprise – from the C-suite to professionals in strategy, analyst relations (AR), market intelligence (MI), business intelligence (BI), product and marketing – to deliver services spanning market data, industry thought leadership and consulting. Our core areas of coverage include AI, Automotive, Consumer Electronics, Displays, eSIM, IoT, Location Platforms, Macroeconomics, Manufacturing, Networks and Infrastructure, Semiconductors, Smartphones and Wearables. Visit our Insights page to explore our publicly available market data, insights and thought leadership, and to understand our focus, meet our analysts and start a conversation.